Payoneer’s China play: CEO John Caplan on Q1 2025 earnings

Payoneer reported solid revenue growth in Q1 2025, though the company has suspended its FY guidance for 2025 amid continued uncertainty around US tariffs. We spoke to CEO John Caplan to find out about the company’s long-term strategy, opening up new total addressable markets and how it sees its China business evolving this year.

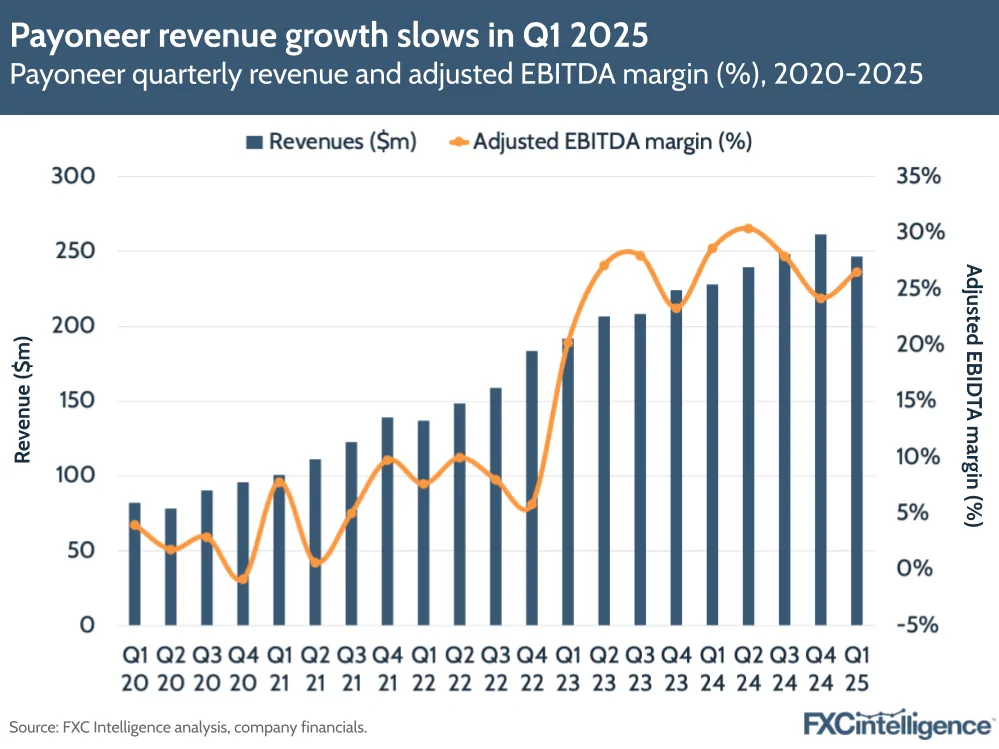

Payoneer continued to report growth in Q1 2025, with revenue excluding interest income rising by 16% to $188.6m and an adjusted EBITDA margin of 27%.

The company has decided to suspend its guidance for FY 2025 on the back of a “high degree of uncertainty around the global macroeconomic and trade policy environment, which is dynamic and evolving”. Near the end of last week, Fortune reported that Payoneer may be looking for a buyer, though the company responded saying that it does not “comment on rumour or speculation”.

Just this week (after Payoneer’s results), the US announced it would be reducing its 145% tariff on Chinese imports to 30%, with China cutting its taxes on imports from 125% to 10%. Significant changes for tariffs in the US were a major talking point for Payoneer’s earnings call last week, given that in 2024 China’s customers accounted for around a third of Payoneer’s revenue. However, during the call the company clarified that 60% of China revenue, or roughly 20% of its total revenue, came from Chinese customers selling to the US.

The company has made some significant inroads in China, having recently become the third foreign entity to be licensed as a payment service provider in the country through its acquisition of Chinese payments firm Easylink Payment. It also continues to see strong diversified growth across other regions – particularly the wider APAC region beyond China and Latin America – and continues to push up take rates by cross-selling products to high-value customers.

In its earnings call, Payoneer said it could see an estimated potential $50m headwind in its 2025 results. However, it stated a roadmap of mid-teens revenue growth with an adjusted EBITDA margin of 25% in the medium term (through 2026), with revenue growth rising to 20%+ in the long term.

We spoke to Payoneer CEO John Caplan to find out more about the company’s China play, as well as key drivers for Q1 2025 and Payoneer’s long-term strategy, with additional comments from VP of Investor Relations Michelle Wang.

Note: Our conversation with John took place before the US government agreed this week to cut its China tariff from 145% to 30% from 14 May over a 90-day period.

Topics covered:

- Payoneer key drivers for Q1 2025 and macroeconomic outlook

- What Payoneer’s China licence means for the business

- How Chinese sellers are staying resilient

- Payoneer’s move into workforce payments

- How Payoneer is making its products stickier

- Building trust with Payoneer customers

Payoneer key drivers for Q1 2025 and macroeconomic outlook

Daniel Webber:

John and Michelle, a pleasure to speak to you again. Take us through the highlights for Payoneer’s Q1 2025 results.

John Caplan:

We delivered another very strong quarter and showed that profitability and innovation can grow hand in hand, even in an uncertain economy. B2B revenue saw 37% year-over-year growth, while ARPU excluding interest was up 22% and has now seen seven quarters of acceleration. Our adjusted EBITDA margin was 27% and adjusted EBITDA excluding interest was $7.5m. This was the fourth quarter of unlocking more leverage in the business.

Our APAC and Latin America regions grew revenue 20% year-over-year, our workforce management acquisition passed $1m of new AR [accounts receivable] and is on the way to solid growth, and we saw an 11 bps take rate expansion in our SMB business.

So in a pre-trade war world, looking at the 16% core business revenue growth and strong adjusted EBITDA margin, we had a very solid Q1. It speaks to the global machine that is Payoneer, which is working well and humming.

On 2 April, we entered a new world of global trade. While there’s disruption in how trade will work and where people will trade, Payoneer is built for the new model of trade where we have teams on the ground in 35 countries.

We disclosed in our earnings update new disclosures that we haven’t shared before. Firstly, a third of our revenue is our China-based customers exporting to the world. We disclosed yesterday that 20% of our revenue is China-based customers selling into the US. That’s important for two reasons. One is we’ve now dimensionalised that and secondly, the China-to-US corridor is very important to Chinese sellers who are selling on Walmart or Amazon or eBay or other platforms, because the US [accounts for] 43% of the world’s consumer demand.

Those high-quality sellers of low-cost goods are essential to the US consumer economy. But even more important in the disclosure – something that’s been an outdated understanding of Payoneer – is that 15% of our revenue today is China sellers selling to Europe or the Middle East or Australia or Latin America.

Today, we are serving businesses in China, exporting to the globe. I don’t think that’s been fully understood and that’s a very important data point. So Chinese sellers are focused on holding their relationships with the ecommerce marketplaces that are so important. They are then accelerating their diversification to the rest of the world and we’re there to support them in doing that.

As it relates to the tariff environment in general and how we’ve communicated, we suspended guidance. In a dynamic and changing environment that’s deeply uncertain to predict – based on the data, the macro environment and the trade dynamic we have today – we sized about a $50m revenue headwind for the second half of the year.

We did that because we think it’s prudent to provide clarity for shareholders and partners around the world about just how strong the pain is here. A business that had guided to a $1bn of revenue sizing a $50m headwind in what is essentially an embargo-like state between China and the US – I think this speaks to just how resilient our business and our P&L is.

Michelle Wang:

I would add that the $50m number is also not meant to be a run rate. In the near-term, the 145% tariff has already been having an impact. Shipping volumes to the ports of Los Angeles are coming down and a lot of people are fearing the shelves will be empty by August when people are going back to school. So yes, there’s a near-term immediate impact, which we’ve sized for.

Longer term however, as trade routes shift there’s going to be benefits as well. The Chinese sellers are incredibly resilient. They will find ways to continue to grow their business and capture opportunity, whether that’s to non-US markets or to re-shift their supply chains and logistics to come to the US via other means.

That will take time of course, and so near-term we’ll see an impact. But the Chinese sellers have been incredibly innovative and, as John says, they are decades ahead of anyone else in terms of manufacturing. It will take them some time to adjust, but we think they will continue to do just fine over the long term.

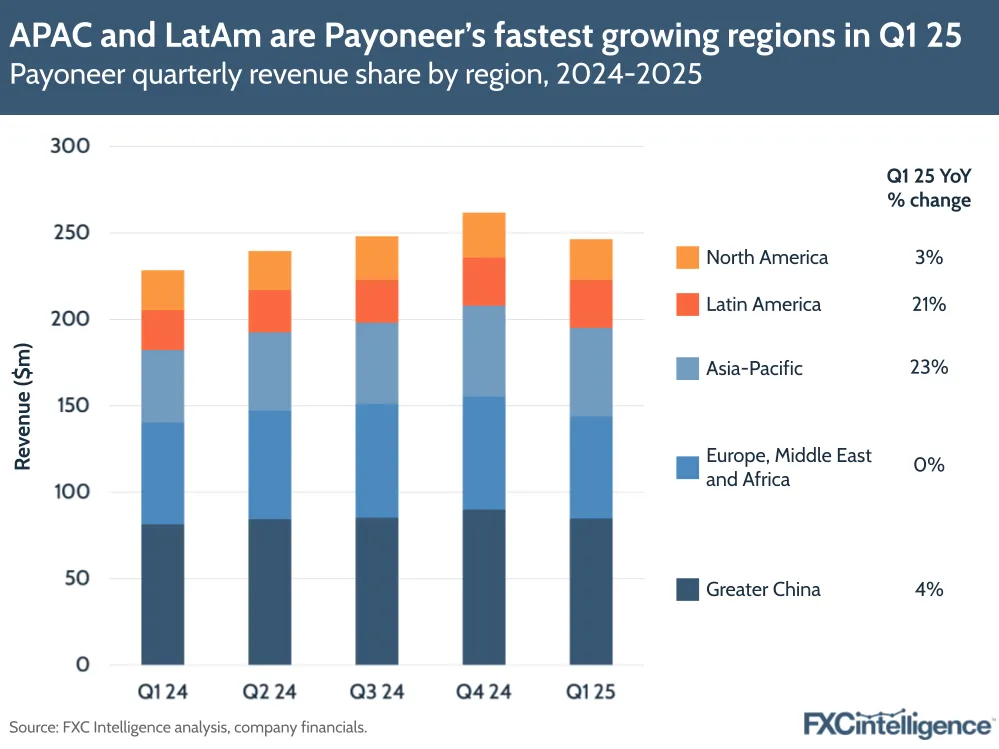

China’s contribution to Payoneer’s revenues

China’s contribution to Payoneer’s revenues has been a key part of the tariff discussion. The company’s Greater China segment (which includes China, Hong Kong, Macao and Taiwan) grew 4% YoY in Q1 2025 and accounted for 34% of revenues.

However, the company is seeing much faster growth in Latin America and APAC, with 21% and 23% YoY growth respectively. Together, these regions now account for around a third of Payoneer’s revenue, and the company expects to see “continued tailwinds as trade routes shift and businesses expand their global footprints”.

Alongside Europe, Middle East and Africa (EMEA), which was flat compared to Q1 2024, no single country included in Latin America and APAC generated more than 10% of total revenue, showing that Payoneer has been able to diversify well in these regions.

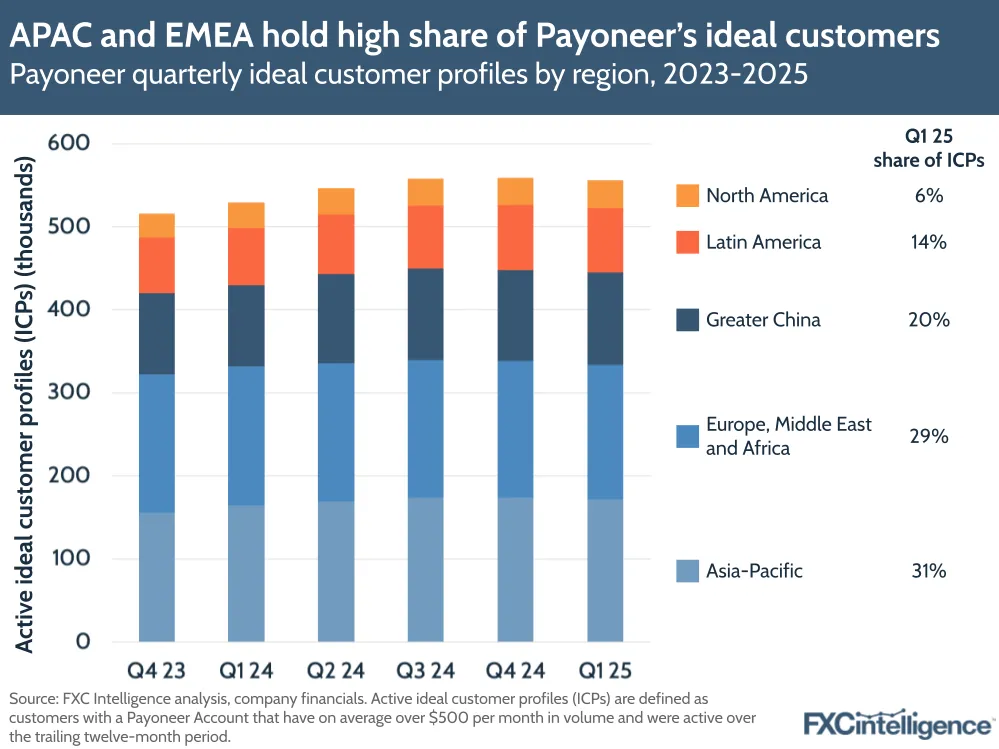

In terms of the breakdown of ICPs – ideal customer profiles, a term for customer segments Payoneer is most focused on growing – across different regions, the breakdown is slightly different to overall revenue. Greater China ICPs accounted for 20% of Payoneer’s total ICPs as of the end of Q1 2025, below APAC and EMEA at 31% and 29% respectively, though higher than Latin America (14%) and North America (6%).

China’s role as a global exporter is tied to its activity, though the diversification of countries and strong growth it is seeing in other geographies could also make the company more resilient in the coming year.

During Payoneer’s earnings call (which took place before the US pullback on tariffs), the company said the existing tariff regime could see a potential headwind to FY 2024 revenues of $50m. However, the company had not seen a slowdown in volumes or revenue in early May and therefore expected growth in Q2 to be broadly in line with medium-term targets.

What Payoneer’s China licence means for the business

Daniel Webber:

You’ve secured a licence in China. What does this mean for Payoneer?

John Caplan:

We’ve built a moat around the Payoneer franchise with our global licensing offices and our relationships with regulators around the world. As we have become the third foreign company to be licensed in China, a few important things come from this. One, we have the ability to expand the services we’re offering to our Chinese customers as they export around the globe. That’s a long-term opportunity for us to pursue.

Secondly, it speaks to how grateful we are to get the licence. It is a significant achievement for our firm and it speaks to the trust that we’ve built over 20 years, the credibility of our organisation and our relationships globally. It’s a significant step forward.

We’re in the process of applying in India and for licences in other parts of the world. Through the course of the next 12 months, we’ll have more announcements to make as we continue to invest in our licensed infrastructure.

Daniel Webber:

As you have already been supporting China sellers, what does the licence allow you to do that you have not been able to do?

Michelle Wang:

It all comes down to being able to more deeply integrate in the local ecosystem. We’ll be able to plug into local payment capabilities rather than go through third-party PSP partners to facilitate the flow of money into China. Over time, this will have expense benefits for us as we can better optimise our costs of sending money into that route. We’ll also be able to put more R&D capabilities on the ground so that we can better localise our products and capabilities in a way that we can’t do without a local licence.

Currently, the business is sending money into China to Chinese sellers, but in the longer term the licence will actually enable us to send money out, which opens up really interesting opportunities in terms of new verticals we can capture over time. For example, helping Chinese travel companies who send Chinese tourists to places like Thailand, who need to send money out of China to pay for Thai hotels and tours.

John Caplan:

Or students who are going abroad. That might be an area of opportunity for us.

Payoneer drives ARPU and EBITDA in Q1 2025

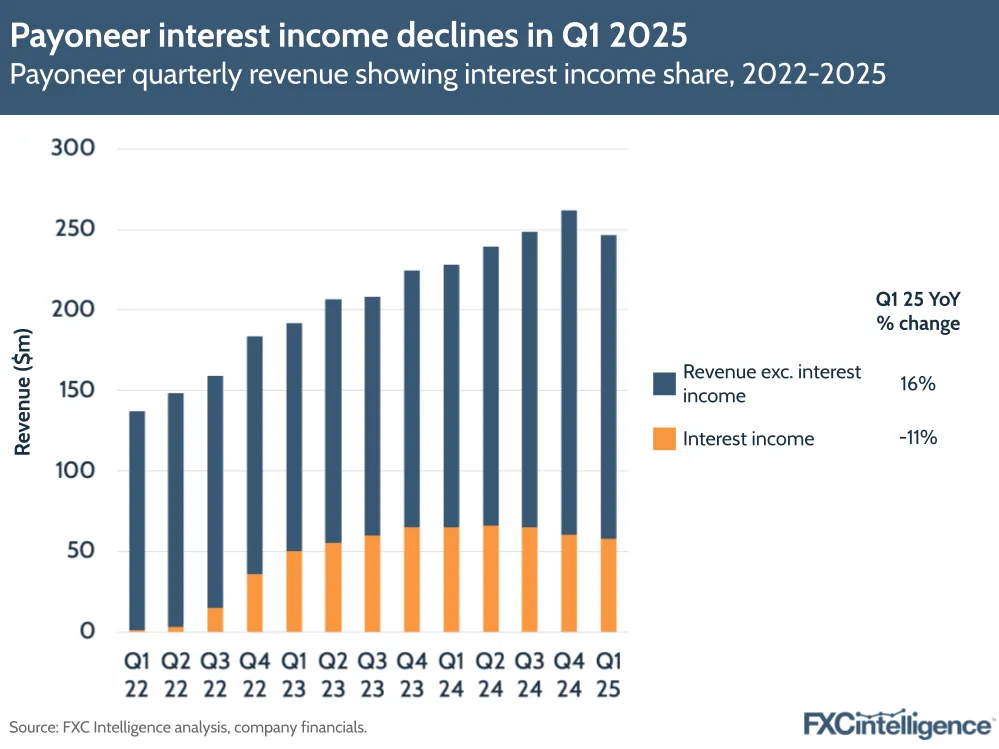

Payoneer saw revenue growth of 8% YoY overall in Q1 2025, slower than previous years, though this accounts for the company’s shifting interest income, which fell by -11% during the quarter.

Excluding interest income (derived from the balances held on its platform), revenue rose 16% during the quarter, which is more aligned with 15% revenue excluding interest income the company saw in Q1 2024, as well as the company’s mid-teens target for the medium term.

Adjusted EBITDA was $65m, with the company saying that this was the highest adjusted EBITDA quarter in nearly three years excluding interest income.

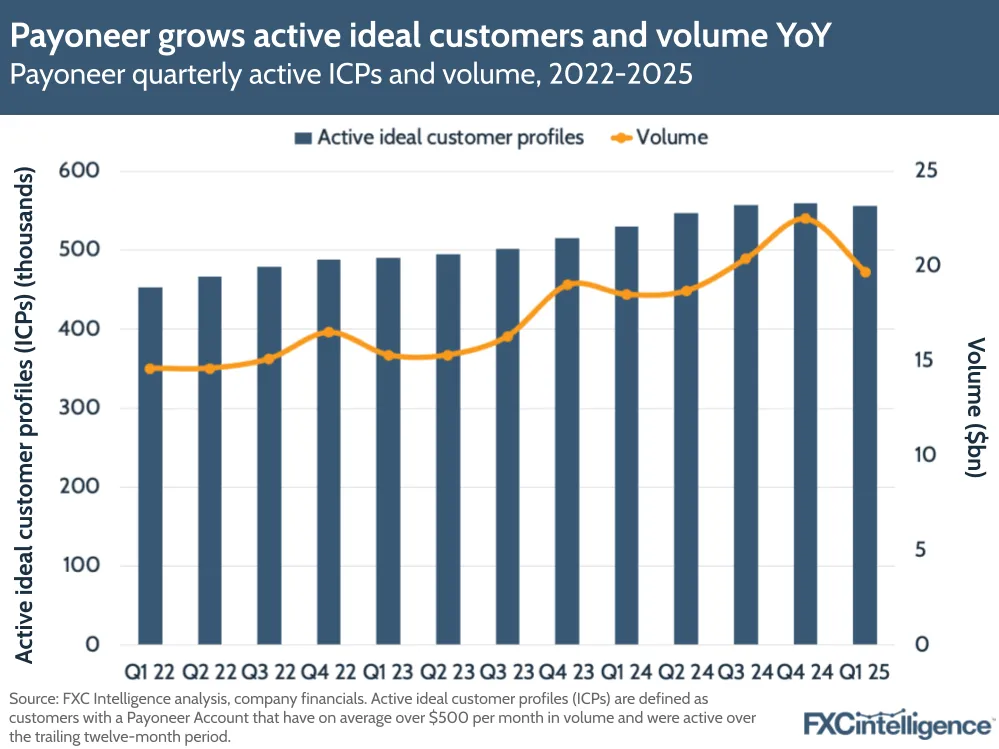

Payoneer continues to build upon its ongoing strategy to target specific high-value users at its company, which account for the vast majority of the company’s revenue. ICPs overall rose 5% to 556,000, helping drive the company’s overall volume up 7%.

Active ICPs that held $500-$10,000 a month rose by 6% to 503,000, though the number of ICPS handling $10,000 a month fell by -7%. Despite this, the larger ICP segment ($10k+ a month) still saw volume grow 8% and revenue up 18%, and is still delivering more than 50% of the company’s revenues. This highlights the company’s strategy of maximising ARPU from its high-value companies through cross-selling its products, as well as driving traction with customers in high-value geographies – such as through the company’s recent acquisition in China.

How Chinese sellers are staying resilient

Daniel Webber:

You know many of these Chinese sellers well from working with them – what are the larger sellers doing to stay resilient?

John Caplan:

They are focused on protecting their relationships with US consumers in the marketplaces. It is very important to Chinese sellers that after the investment they’ve made and the relationships they’ve built, to continue to sell. The next thing is they are diversifying their supply chains. They’re looking to set up manufacturing capabilities outside of China and exploring Vietnam, Thailand, Bangladesh and other parts of the world.

With the US’s de minimus exemption going away, they are also moving pallets and container loads of product forward as opposed to shipping individual sleeves of product. They’re also adjusting their pricing and considering how much elasticity they have in the price of the product they are selling. And then they are sunsetting products that maybe were less profitable or interesting, or more competitive, and investing behind uniqueness and differentiation.

Most importantly, this trade conflict has become a forcing function for globalising distribution of Chinese sellers. They are very focused on Europe, Latin America, APAC and the Middle East. What’s happened is a wake-up call to say we need to make our businesses even more global and diverse. From Payoneer’s perspective, it actually makes our products and the multicurrency nature of them more valuable to our customers, as we provide a single account where you receive your AR from multiple global marketplaces. So, we are sort of arm in arm with them as they go global.

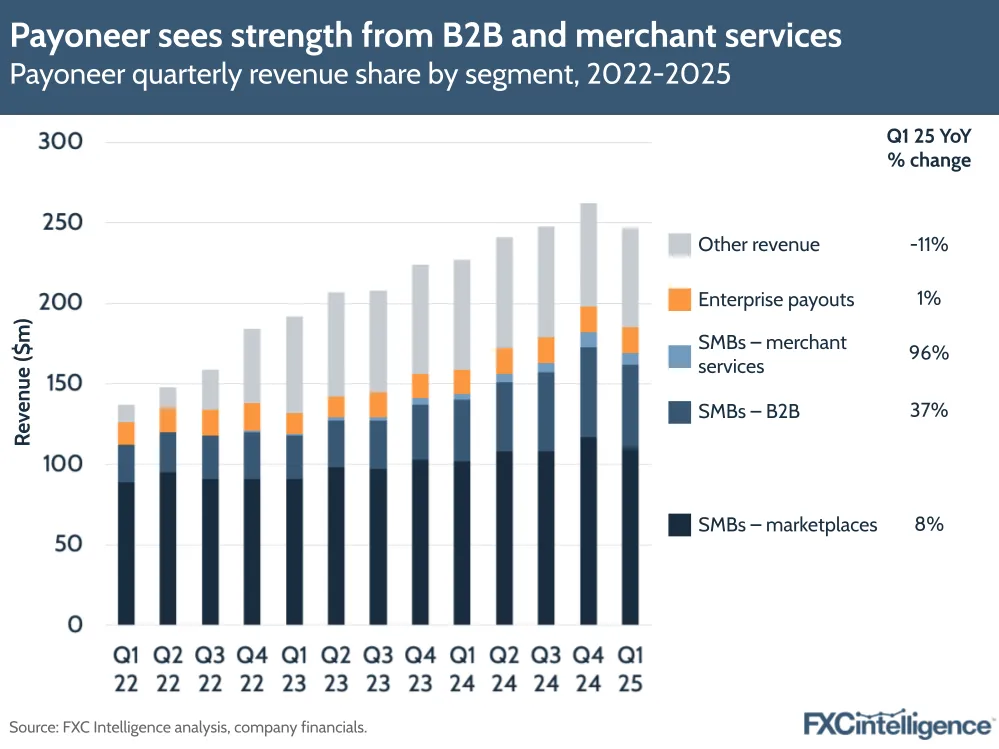

B2B payments continue to drive Payoneer’s growth

B2B payments, and in particular SMB payments, continue to be Payoneer’s biggest revenue stream, though the company has reclassified them slightly in Q1 2025. In particular, “certain non-volume revenues including those related to banking partnerships and FX that were previously allocated to SMBs selling on marketplaces were re-classified to B2B SMBs to better reflect the customers supporting those revenues”.

With the new system, SMBs selling on marketplaces saw 8% YoY growth and still contained the highest revenue share at $110m, though they were significantly outpaced on growth by B2B SMBs, which grew 37% to $52, and merchant services, which grew 96% to $7m. Overall, SMB revenues rose 18% vs 1% growth for enterprise payouts.

Payoneer’s move into workforce payments

Daniel Webber:

Outside of China, what have been the key drivers for Payoneer in Q1 2025?

John Caplan:

We have a great tailwind in Latin America and APAC, where we saw greater than 20% revenue growth in Q1. We feel very good about the teams, the execution and the opportunity in these environments.

Secondly, our workforce management acquisition is working and it’s proof that the companies in the US, but really around the world, are hiring talent all over the world, and increasingly choosing Payoneer as a solution to pay their employees and contractors globally. This is TAM-expanding for us and a really powerful step forward, and it proves the cross-sell new customer acquisition effort that’s underway.

Daniel Webber:

What drove Payoneer to make this workforce management acquisition, and what has it now unlocked for you?

John Caplan:

We’ve been helping people pay contractors globally for a decade. That’s part of our brand – our relationship with Fiverr and Upwork, and the freelance economy. What this opened up specifically was it expanded our software capability in that arena, and then opened up employer-of-record opportunities.

For example, if you, Daniel, hired somebody in Switzerland, I would hire them and subcontract them to you so that I’m the technical employer, and you pay me every month to manage that service for you.

That’s working for us and we’re trusted to do that. It’s a complex regulated business globally because it’s employment law around the world, so it’s hard to get into. Once you have a beachhead there, there are lots of expansion opportunities.

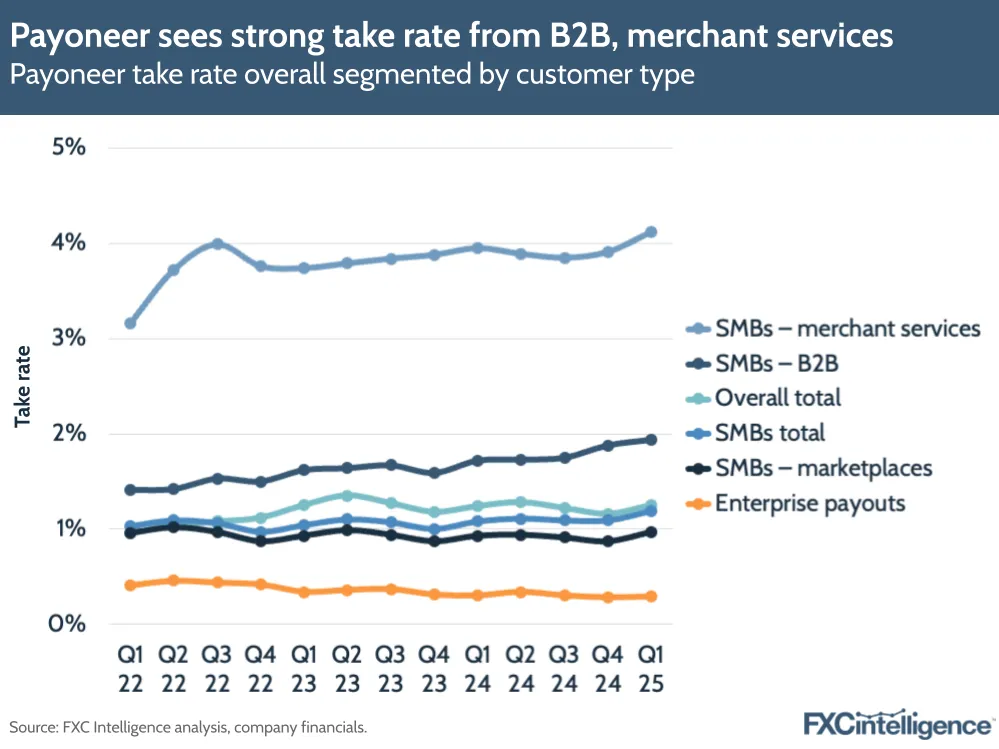

Payoneer’s growing SMB take rate

A key driver for Payoneer has been significant take rate expansion with SMB customers, with the company’s take rate for these customers growing 11 bps to 1.19%. Once again, B2B SMBs and merchant services were key to growing this figure, with the former seeing its take rate rise 22 bps to 1.94% while merchant services’ rate grew 17 bps to 4.12%.

The take rate rises highlight that the company is capturing more value from its markets, which as the company put it in the earnings call, is helping it “outrun the impact of lower interest income”. It’s been driven by Payoneer’s continued growth in its B2B franchise, adoption of high-value products and various pricing initiatives, as well as the impact of the company’s workforce management acquisition.

How Payoneer is making its products stickier

Daniel Webber: You mentioned that 53% of customers now use three or more of Payoneer’s AP [accounts payable] products. What are some of the other products people are using?

John Caplan:

A good example is our card products. We’ve seen really exceptional growth in Latin America with customers choosing to get paid into Payoneer accounts and then using the Payoneer card for their travel expenses as their employees go travelling. That would be a use case.

As an example, we have Pay with Payoneer, where customers are receiving funds into their Payoneer account and then paying for raw materials straight out of the account from suppliers across Asia. That’s a product that’s seen really strong adoption.

Another one is invoicing capabilities. We’ve seen that the more invoices somebody sends and the higher average ticket value they send, the stickier the product becomes. More and more so we’re sort of an office of the CFO solution or a business owner that’s operating in multiple geographies.

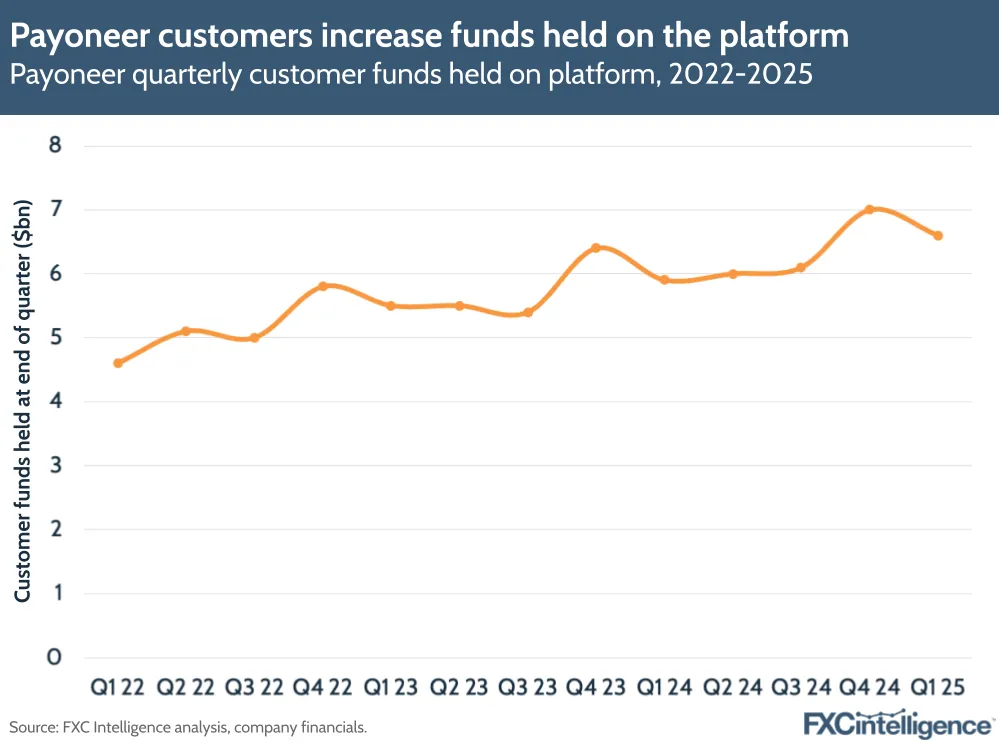

Payoneer customers grow funds on the platform

As Payoneer has built out its network and added new customers, it often points to the value of money being held on its platform as an indicator of trust in the business. Customer funds grew by 11% YoY to $6.6bn, which the company attributes to the importance of its multicurrency accounts for doing business and making payments globally.

In turn, Payoneer says, rising funds on the platform are helping offset aforementioned declines in interest income due to lowering average interest rates, though interest income still accounted for 24% of Payoneer’s overall revenue figure in Q1 25.

The company says it had also implemented various measures to reduce its sensitivity to changing short-term interests in relation to $3.7bn (approximately 56% of customers’ funds), and continues to actively manage its hedging programmes.

Building trust with Payoneer customers

Daniel Webber:

You had over $6.6bn of customer balance, which is also a nice sign of the trust that continues to grow.

John Caplan:

Holding a multicurrency account and keeping the balances with Payoneer while you’re not earning any yield, tells the story of how valuable the account is and how trusted we are.

Here is something that has been surprising to US-based investors: with all the financial technology we all have access to and the relationships we have with our banks, we’re a unique solution for a thousand person business in Serbia that has employees across Europe. We’re a unique solution for somebody in Colombia who’s doing business to Ecuador. We’re moving money from Ecuador to Colombia and it costs up to 30%. So our 2% feels pretty efficient.

There’s short-term disruption, but we’re more confident long-term about what we’re building. That’s genuinely how our leadership team feels about where we are.

Daniel Webber:

John, Michelle, thank you.

John Caplan and Michelle Wang:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.